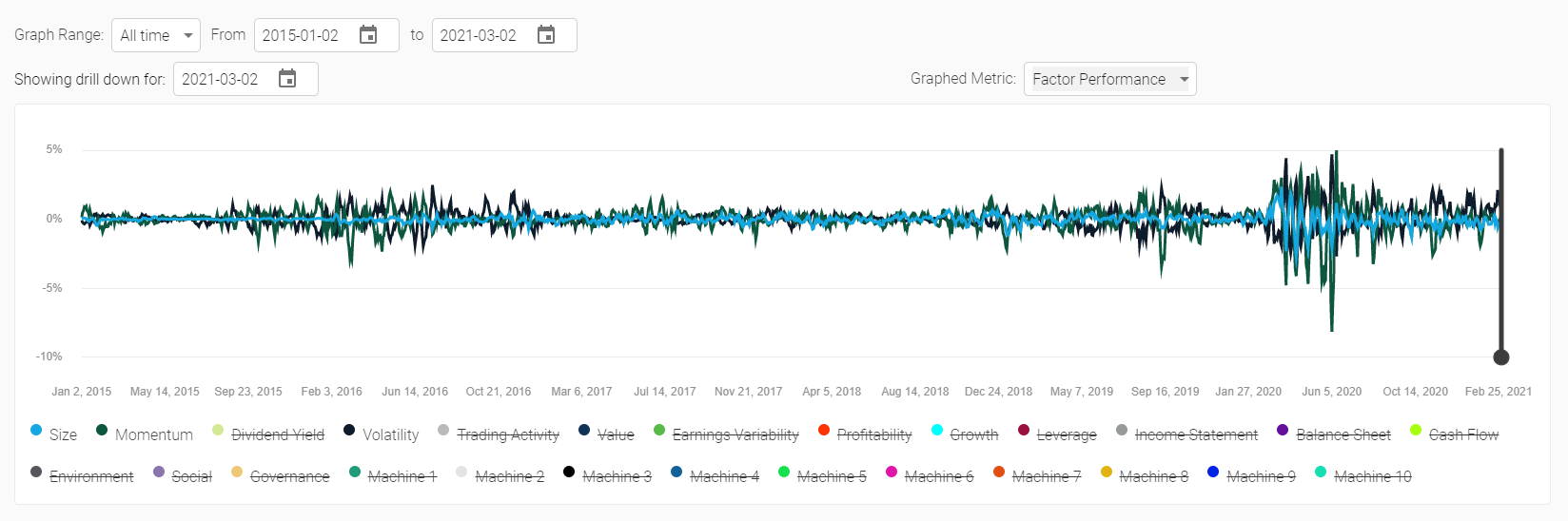

Factor performance shows how much of the trailing 5 day excess return can be attributed to each factor. For example, if Momentum shows a value of 1% that means that your portfolio gained 1% in value (relative to the equal weighted benchmark of your universe) due to its exposure to the Momentum factor. Importantly, this could be a result of either an under or an over exposure to the factor. If you had a Momentum exposure of -100% and Momentum underperformed by 1% then you would see a positive gain of 1% due to your Momentum factor exposure.